Climate Change (Information Disclosure Based on TCFD Recommendations)

Primary contents from here.

Climate Change (Information Disclosure Based on TCFD Recommendations)

In May 2019, ITOCHU announced our support for the TCFD* recommendations in recognition of the importance of climate-related financial disclosures. Since then, we continue working to provide information disclosure based on TCFD recommendations.

TCFD: The Task Force on Climate-related Financial Disclosures established by the Financial Stability Board (FSB).

Policy and Basic Concept Concerning Climate Change

ITOCHU recognizes that climate change is one of the most urgent global environmental issues, therefore ITOCHU Group, which operates globally, considers climate change and other global environmental issues as one of the most important management issues. We support international policies and standards, including the Paris Agreement, Japan’s NDC (Nationally Determined Contribution), climate change-related laws and regulations (such as the Act on Rationalizing Energy Use and the Act on Promotion of Global Warming Countermeasures) and various governmental policies, and we will view adaptation to changes in the business environment due to climate change as an opportunity for further growth and incorporate these into our policies and specific initiatives.

We define our initiatives related to climate change in the ITOCHU Group Environmental Activities Policies “2. Response to Climate Change: We shall reduce greenhouse gas (GHG) emissions and increase the efficiency of energy use within our own operations, as well as externally provide products and services that contribute to the mitigation and adaptation to climate change.” In March 2021, our Board of Directors approved the inclusion of GHG emissions reduction targets for 2030, 2040, and by 2050 as core targets for our medium-term management plan, Brand-new Deal 2023. These targets are in line with Japan’s NDC, which we aim to achieve by reducing avoidable emissions and actively promoting businesses that contribute to reductions. Under our corporate philosophy of the Sampo-yoshi approach, we will respond to climate change risks and opportunities in collaboration with the stakeholders to increase our corporate value.

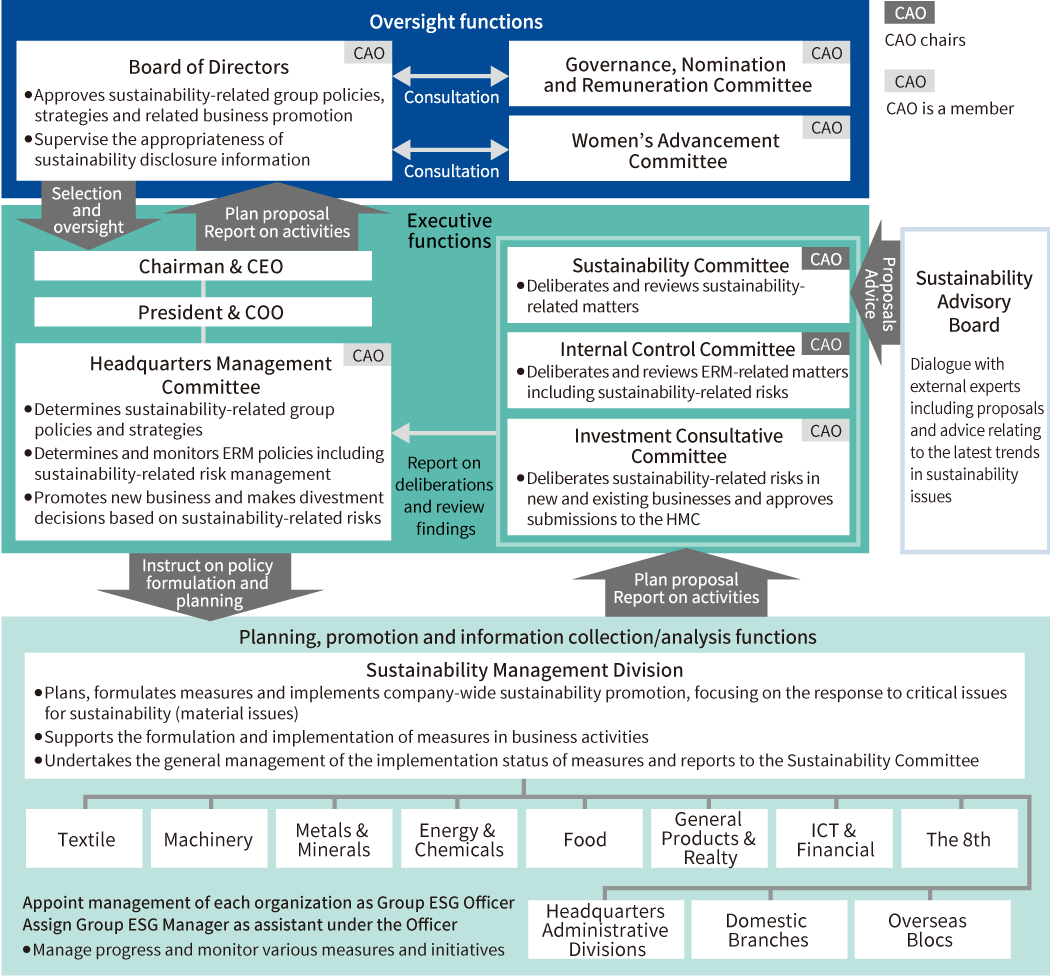

Governance

ITOCHU views responding to climate change and other sustainability issues as an important management issue. Our Board of Directors gives due consideration to response policies for climate change-related risks and opportunities and GHG reduction targets and initiatives, and incorporates these policies into deliberations and decisions on annual budgets, business plans, and other core matters.

The ITOCHU Sustainability Committee is the body delegated with general management responsibilities concerning the proposal and implementation of the various policies that will enable us to respond to climate change and other sustainability matters. This Committee ascertains, manages, and evaluates climate-related targets, the implementation status of transition plans, and current environmental and social risks and opportunities. ITOCHU’s Chief Administrative Officer (CAO) is the director responsible for climate-related issues and is also a member of the Headquarters Management Committee (HMC). The CAO also serves as chair of the Sustainability Committee. The CAO provides a report to the Board of Directors approximately twice per year on matters deliberated and decided by the Sustainability Committee in addition to a report on the status of major sustainability promotion activities. This creates an organization that allows the Board of Directors to appropriately supervise business and financial strategies (including reviewing strategy and making divestment and asset replacement decisions) for responding to environmental and social risks and opportunities while giving proper consideration to matters deliberated and decided by the Sustainability Committee. As the executive level, management from each Company and administrative division also serving as ESG Officers participate in Sustainability Committee meetings as core members. The Sustainability Committee receives reports on climate-related matters from the Sustainability Management Division and ESG Managers from each Company and administrative division. We use these reports towards progress management and monitoring for each policy and various initiatives.

In 2021, our Board of Directors approved the inclusion of growth strategy and GHG emissions reduction targets in our medium-term management plan, Brand-new Deal 2023. This decision reflects our commitment to the climate-related issues impacting our Company and we believe this will enable us to lead the industry in realizing a decarbonized society in enhancing our contribution to and engagement with the SDGs through business activities. Based on this decision by the Board of Directors, the Sustainability Committee deliberates specific policies and targets related to decarbonized initiatives. Each business division works continuously to implement these policies and initiatives approved by the CAO, the director in charge, and progress is reviewed by the Sustainability Committee. Our Board of Directors has further resolved to continuously respond to social demand by aiming to balance both sustaining the basic policies outlined in the previous medium-term management plan and to promote businesses that contribute to emissions reduction and reflected it in the Management Policy “The Brand-new Deal” formulated in 2024.

The chair of the Sustainability Committee and management from each Company and administrative division (ESG Officers) meet with external experts (a Sustainability Advisory Board) once a year to engage in dialogue towards making continuous improvements to our response to climate change and other sustainability issues. Through this dialogue, we promote climate change countermeasures based on an understanding of society’s expectations and demands on ITOCHU.

Governance System Concerning Climate Change (As of June 18, 2025)

Climate-related Meetings Held by the Board of Directors and Committees

Frequency of Meetings and Reports

Main Items Deliberated or Reported on (FYE 2019 to FYE 2025)

The Board of Directors

Periodic reports are made at least once a year

Results

Once in FYE 2019

2 times in FYE 2020

Once in FYE 2021

2 times in FYE 2022

3 times in FYE 2023

4 times in FYE 2024

3 times in FYE 2025

FYE 2019

Announcement of support for the TCFD recommendations

FYE 2020

Disclosure based on the TCFD recommendations, calculation of Scope3 emissions

FYE 2021

GHG reduction target, Disclosure based on the TCFD recommendations

FYE 2022

Creation of medium-term management plan, Brand-new Deal 2023. (Growth strategy and GHG emissions reduction targets towards leading the industry in realizing a decarbonized society in enhancing our contribution to and engagement with the SDGs through business activities.)

Report on ITOCHU SDGs/ESG initiatives

FYE 2023

Confirmation of the Material Issues

Policy for GHG emissions reduction

Monitoring of Scope1/2/3 results

FYE 2024

Status of GHG emissions reduction roadmap

Results and forecast of avoided emissions

FYE 2025

Response to new information disclosure requests

Response to climate change

Response to natural capital

Sustainability Committee

Usually held 1 to 2 times a year

Results

Once in FYE 2019

2 times in FYE 2020

Once in FYE 2021

Once in FYE 2022

3 times in FYE 2023

3 times in FYE 2024

2 times in FYE 2025

FYE 2019

Announcement of support for the TCFD recommendations

FYE 2020

Disclosure based on the TCFD recommendations, calculation of Scope3 emissions

FYE 2021

GHG reduction target, Disclosure based on the TCFD recommendations

FYE 2022

Confirmation of Scope1/2/3 results, status of progress on reduction targets

FYE 2023

Confirmation of the Material Issues

Policy for GHG emissions reduction

Monitoring of Scope1/2/3 results

FYE 2024

Status of GHG emissions reduction roadmap

Results and forecast of avoided emissions

FYE 2025

Revision of The ITOCHU Group Environmental Policy

Revision of Sustainability Action Guidelines for Supply Chains and expansion of distribution

GHG-related reporting

Strategy

ITOCHU applies the Policy and Basic Concept Concerning Climate Change to analyze scenarios based on TCFD recommendations (analysis of transition and physical risks and opportunities associated with climate change). We use the results of these analyses to realign our business strategy and portfolio.

Climate-related Risks and Opportunities

ITOCHU is engaged in various businesses in locations around the world. Each business is impacted by various short-, medium-, and long-term climate change transition risks and physical risks. As such, ITOCHU globally identifies, evaluates, and manages risks and opportunities with the possibility to have a material financial impact on our business, supply chain, and strategy. We conduct such analysis and evaluation throughout each business proposal management process and in our environmental and social risk management processes, which includes climate change.

Please scroll sideways.

Material Climate-related Risks and Opportunities (risk criteria)

Climate-Related Risks and Opportunities

Impact of Climate-related Risks and Opportunities on the Organization’s Business, Strategy, and Financial Planning

Impact Timeline*

Impacted Value Chains

Related Businesses

Transition Risks and Opportunities

Policy and Legal Systems

If countries around the world take a more aggressive approach in their GHG emissions reduction targets and subsequently strengthen laws and regulations regarding corporate emissions, fossil fuel demand may see a sharp decrease.

Increased operating costs due to carbon pricing (carbon tax, etc.) or business regulations

Medium-term Long-term

Upstream, ITOCHU Group

Power generation business, Fossil fuel business, Iron ore business, Automobile business, Chemicals business

Technical Innovation

Business opportunities that contribute to mitigation to climate change are expected to increase (e.g., renewable energy, energy storage systems, low-carbon fuels, low-carbon emission steelmaking raw materials, etc.)

Short-term Medium-term Long-term

ITOCHU Group

Renewable energy, Energy storage system businesses, Low-carbon fuel business, New material business, Iron ore business

Changes in Market Conditions

Demand for certain products and services may increase or decrease due to market risks related to public policy, laws and regulations, or technological advancements (e.g. clean technology)

Short-term Medium-term Long-term

Upstream, ITOCHU Group

Fossil fuel business, Chemicals business, Automobile business, Renewable energy, Energy storage systems businesses, New material business, CCUS/emissions credit-related businesses

Physical Risks and Opportunities

Acute Physical Risks and Opportunities

Operations may be impacted or damaged by increased occurrences of extreme weather patterns (e.g., droughts, floods, typhoons, hurricanes, etc.)

Short-term Medium-term Long-term

Upstream, ITOCHU Group, downstream

Food business, Forestry-related businesses, Mining business

We may be able to strengthen customer retention and/or attraction by strengthening our supply chain resilient to extreme weather patterns and promoting stable supply as a value proposition

Short-term Medium-term Long-term

Upstream, ITOCHU Group, downstream

Food business, Forestry-related businesses

Chronic Physical Risks and Opportunities

Our capability to maintain and increase the quantity of agricultural and forestry-related harvests, as well as products manufactured using these yields, may be impacted by climate-related changes such as increasing temperatures and likelihood of droughts.

Medium-term Long-term

Upstream, ITOCHU Group, downstream

Food business, Forestry-related businesses

Short-term: less than one year, medium-term, up to three years, long-term: four or more years

Scenario Analysis

Scenario Selection

ITOCHU categorized our businesses with climate impact, such as GHG emissions volume on the vertical axis and climate-related financial impact on the horizontal axis and analyzed our businesses with priority given to those mapped in a zone where both dimensions are high. Based on this, we designated the following businesses as targets for scenario analysis: “Power Generation,” “Energy,” “Coal-related,” “Iron Ore,” “Automobile,” and “Chemicals” as businesses with significant transition risk impacts, including policy and legal risks, and “Dole,” “Feed and Grain Trade,” and “Pulp” as businesses with significant physical risk impacts from climate change. The above nine businesses are included in the four non-financial sectors (energy, transportation, materials and buildings, and agriculture, food, and forest products) designated by the TCFD as potentially highly affected by climate change.

When considering ITOCHU scenario analysis, we referenced materials published by the International Energy Agency (IEA) and the Intergovernmental Panel on Climate Change (IPCC). These materials are highly recognized internationally for their credibility, are referenced in TCFD recommendations, and cover a broad range of business domains. As a result, we set the following two scenarios.

As the reduction targets of various countries, international guidelines, and investor demands are mainstreaming the goal of limiting the increase to 1.5℃ above pre-industrial levels, we will continuously review the risks, opportunities, and mitigation measures based on the parameters and business environment approximately every 1 to 2 years.

Please scroll sideways.

Scenario

4℃

1.5℃

Image of society

The policies of countries, such as the Intended Nationally Determined Contributions (INDC) established in accordance with the Paris Agreement, are implemented. Nevertheless, the average temperature at the end of this century rises by 4℃. This is a society in which there is a high likelihood climate change (e.g., a rise in temperature) will impact business.

Bold policies and technological innovations will be promoted to limit the average temperature increase to 1.5℃ until the end of the century and achieve sustainable development. This is a society in which social changes due to the transition to a de-carbonized society are highly likely to impact business.

Reference scenarios

Transition aspects

Stated Policies Scenario (IEA WEO2024*)

Stated Policies Scenario (ETP WEO2020), etc.

Net Zero Emissions by 2050 Scenario (IEA WEO2024)

Announced Pledges Scenario (IEA WEO2024), etc.

Physical aspects

RCP8.5 (IPCC AR5), SSP5-8.5 (IPCC AR6), etc.

RCP2.6 (IPCC AR5), SSP1-1.9, SSP1-2.6 (IPCCAR6), etc.

Risks and opportunities

Risks and opportunities in terms of physical aspects will be more likely to surface

Risks and opportunities in terms of transition aspects will be more likely to surface

IEA WEO2024 “Net Zero Emissions by 2050 Scenario”: A scenario that shows a possible path for the global energy sector to achieve net zero GHG emissions by 2050 and limit temperature rise to 1.5℃ above pre-industrial levels.

Important Input Parameters and Prerequisites for the Climate-related Scenarios

Important input parameters and prerequisites for the climate-related scenarios we used include the following types of parameters.

Please scroll sideways.

Parameters Used to the Power Generation Business in the US

Timeframe: By 2040

4℃ Scenario

1.5℃ Scenario

Carbon price

N/A

US$205/t-CO2

Thermal power generation

Coal: 5,650TWh

Gas: 6,405TWh

Coal: ―

Gas: 1,256TWh

Renewable energy generation

Solar: 14,912TWh

Wind: 9,492TWh

Geothermal: 271TWh

Solar Heat: 115TWh

Solar: 24,846TWh

Wind: 17,293TWh

Geothermal: 529TWh

Solar Heat: 731TWh

Low-carbon thermal power generation

Hydrogen and ammonia: 80TWh

Thermal power with CCUS: 79TWh

Hydrogen and ammonia: 878TWh

Thermal power with CCUS: 833TWh

Scenario Analysis and Results

For the scenario analysis, ITOCHU did not limit the timeline range to the short-term. We also added medium- and long-term axes for 2030 and beyond when organizing and evaluating the factors of latent risks and opportunities that could have a significant qualitative or quantitative financial impact for each business. We identified risk and opportunity factors from the perspective of procurement, business operations, and markets’ demand for the subject business, and then organized and evaluated factors of high importance. For particularly important factors, our scenario analysis was based on financial models that reflect defined parameters. We defined these parameters by identifying variables that significantly impact transition and physical risks and opportunities. For the analysis of financial impact level, we measured the latent impact level of climate change and analyzed the financial impact level, including the effect of risk and opportunity measures.

The quantitative information used in our scenario analysis reflects judgments made by ITOCHU based on scenarios prepared by sources such as the IEA. While we worked to increase analysis precision, the analysis does include numerous uncertainties.

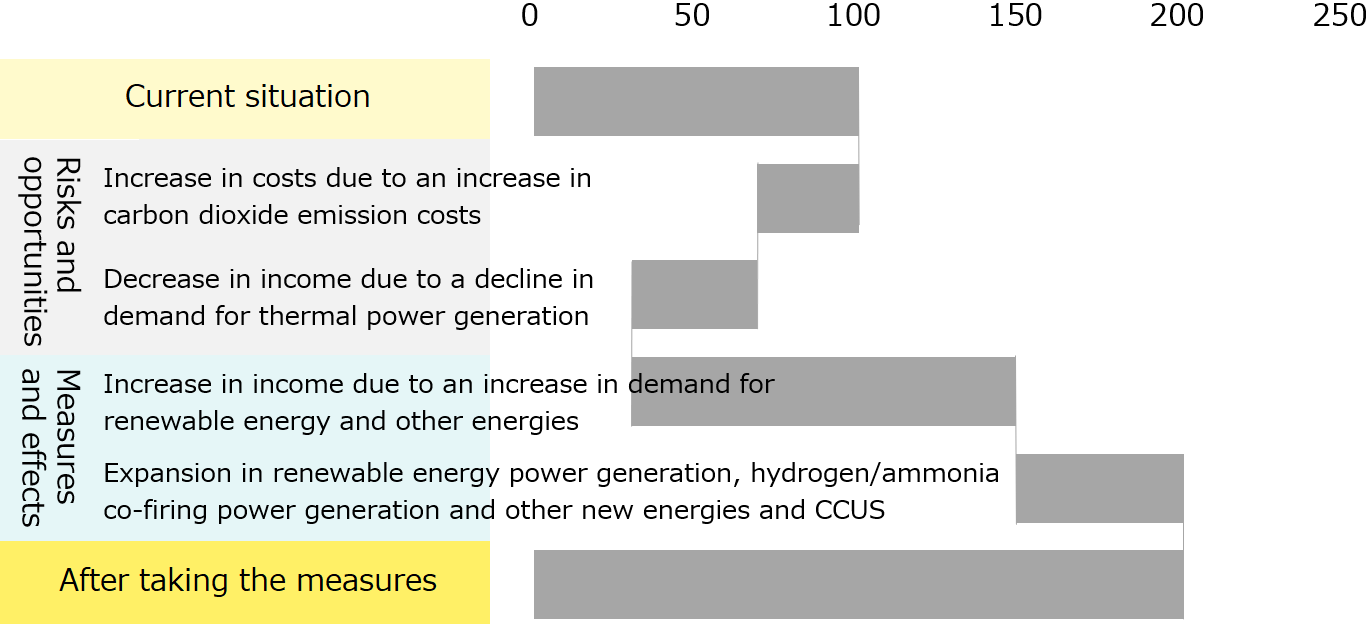

1. Businesses for Which Transition Risks Are the Main Issues

The main issues for following six business are transition risks in the 1.5℃ scenario.

Risk: Decrease in thermal power station earnings due to effects such as an increase in carbon dioxide emission costs

Risk: Decline in demand for thermal power generation

Opportunity: Improvement in profitability due to an expansion in renewable energy business opportunities, technological advances and cost reductions

Opportunity: Increase in earnings due to the increased use of hydrogen/ammonia co-firing power generation, CCUS and other technologies

Physical

Risk: Damage to power generation facilities by natural disasters (extreme weather)

Business environment under the scenario Business impact assessment

Earnings may decrease due to an increase in carbon dioxide emission costs and a decline in demand for thermal power generation in the transition scenario. On the other hand, earnings are expected to increase overall due to an expansion in new energies including renewable energy power generation, hydrogen/ammonia co-firing power generation and CCUS.

Analysis according to the EBITDA indicator (%)*

Earnings before interest, taxes, depreciation and amortization (This refers to earnings calculated by adding interest expenses and depreciation expenses to earnings before tax.)

Adaptation/mitigation measures & policies

Business opportunities

We aim to have a renewable energy ratio of over 20% (equity interest basis) by FYE 2031. We will reflect this aim in our future initiatives.

We will not develop new coal-fired power generation projects to contribute to the building of a sustainable society.

Financial information

Profit in segment of applicable business (consolidated net profit): 56.9 bn yen (Plant Project, Marine & Aerospace Division/FYE 2025 Results)

Total assets in segment of applicable business: 2,166.6 bn yen (Machinery Company/March 2025)

Timeframe

By 2030

Temperature Band Scenario

1.5℃ Scenario

Main risks and opportunities

Transition

Risk: The number of internal combustion engine vehicles we handle may decrease

Opportunity: The number of electric vehicles we handle may increase

Opportunity: New business may expand with the spread of electric vehicles

Risk: Transportation costs may rise due to the introduction of carbon taxes

Physical

Risk: There is a risk the factories of our business partners may suffer damage and suspend operations

Business environment under the scenario Business impact assessment

The automobile industry is shifting from internal combustion engine vehicles to electric vehicles. Our customers are found all over the world. That means we can expect automobile demand to remain firm despite the expectation there will be a gradual shift in the vehicles we handle from internal combustion engine vehicles to electric vehicles in line with the regulations of each country. It is also expected that the introduction of carbon taxes may lead to an increase in transportation costs in some regions. We will continue to maintain competitiveness by working with our partners to reduce costs. We will aim to obtain further earnings by strengthening our storage battery and other related businesses with the spread of electric vehicles.

Analysis according to the Gross trading profit indicator (%)

Adaptation/mitigation measures & policies

Business opportunities

We will continue to expand business by ascertaining demand trends by region based on the electric vehicle development and production situation of automobile manufacturers and trends in electric vehicle-related regulations in the countries where we sell our products.

We will strengthen relationships with business partners who are reducing GHG in regard to freight forwarders and marine transportation companies.

We will develop and expand business by linking up with partners who are mainly automobile manufacturers to expand our electric vehicle-related business.

Financial information

Profit in segment of applicable business (consolidated net profit): 79.6 bn yen (Automobile, Construction Machinery & Industrial Machinery Division/FYE 2025 Results)

Total assets in segment of applicable business: 2,166.6 bn yen (Machinery Company/March 2025)

Timeframe

By 2050

Temperature Band Scenario

1.5℃ Scenario

Main risks and opportunities

Transition

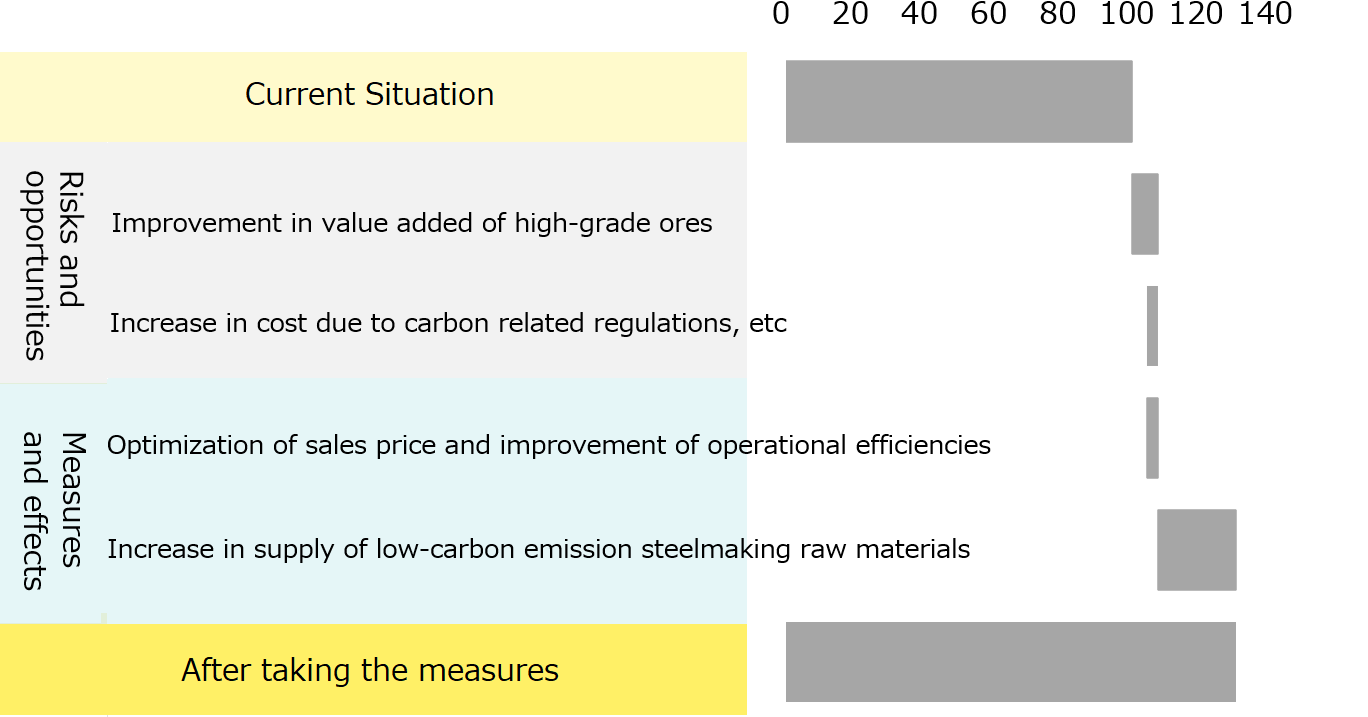

Opportunity: Improvement in value added of high-grade ores

Risk: Increase in cost due to carbon related regulations, etc

Opportunity: Optimization of sales price and improvement of operational efficiencies

Opportunity: Increase in supply of low-carbon emission steelmaking raw materials

Physical

Risk: Disruption of the iron ore supply chain due to frequent weather disasters

Business environment under the scenario Business impact assessment

Carbon related regulations are expected to increase cost such as the purchase of emission credits rights according to GHG emissions. Nevertheless, the impact on earnings will be limited due to optimization of sales prices in iron ore supply chain and improvement of operational efficiencies including policy to reduce GHG emissions and promotion of digital transformation, etc. Further growth is expected by strengthening the production of high-grade ore, for which demand is expected to increase due to the acceleration of the shift to decarbonization, and steadily seizing business opportunities in iron ore and related fields, such as creation of businesses related to low-carbon emission steelmaking raw materials.

Analysis according to the profit after tax (%)

Adaptation/mitigation measures & policies

Business opportunities

We will closely monitor trends in low-carbon emission steelmaking technologies and promote initiatives to ensure a stable supply of low-carbon emission steelmaking raw materials.

We will promote initiatives to improve operational efficiencies including policy to reduce GHG emissions and digital transformation.

Financial information

Profit in segment of applicable business (consolidated net profit): 178.4 bn yen (Metals & Minerals Company/FYE 2025 Results)

Total assets in segment of applicable business: 1,506.4 bn yen (Metals & Minerals Company/March 2025)

Timeframe

By 2040

Temperature Band Scenario

1.5℃ Scenario

Main risks and opportunities

Transition

Risk: Transition of coking coal demand

Opportunity: Rising scarcity of high-grade coking coal, which is essential for the low-carbon steelmaking processes

Risk: Increase in cost due to carbon related regulations, etc

Opportunity: Optimization of sales price and improvement of operational efficiencies

Opportunity: Capture of coal-related business opportunities that contribute to low carbonization such as hydrogen, CCUS, etc

Physical

Risk: Disruption of the coal supply chain due to frequent weather disasters

Business environment under the scenario Business impact assessment

Under 1.5℃ Scenario overall demand for coking coal is expected to decrease due to the advancement of electric furnaces and the spread of direct reduced iron. On the other hand, the number of coal mines capable of supplying high-quality high-grade coking coal will become more limited than before, and such coal is needed not only for the conventional blast furnace method but also for the blast furnace hydrogen reduction process, so it is expected to become relatively scarce. Carbon related regulations are expected to increase cost such as the purchase of emission credits rights according to GHG emissions. Nevertheless, the impact on earnings will be mitigated due to optimization of sales prices in coal supply chain and improvement of operational efficiencies including policy to reduce GHG emissions and promotion of digital transformation, etc. In the medium and long term we will aim to maintain and expand profits by capturing business opportunities in coal-related fields, such as CCUS (Carbon dioxide Capture, Utilization and Storage), which includes promoting the spread of CO2 fixation technology, and hydrogen utilization, etc.

Analysis according to the profit after tax (%)

Adaptation/mitigation measures & policies

Business opportunities

Regarding high-grade coal, which contributes to the low-carbonization of steel, we are expanding supply from superior interests while improving asset efficiency.

We will promote initiatives to improve operational efficiencies including policy to reduce GHG emissions and digital transformation.

We will closely monitor trends in low-carbon emission steelmaking technologies and capture business opportunities in coal-related fields that contribute to the low-carbonization of related industries, while identifying changes in social structure.

Financial information

Profit in segment of applicable business (consolidated net profit): 178.4 bn yen (Metals & Minerals Company/FYE 2025 Results)

Total assets in segment of applicable business: 1,506.4 bn yen (Metals & Minerals Company/March 2025)

Timeframe

By 2040

Temperature Band Scenario

1.5℃ Scenario

Main risks and opportunities

Transition

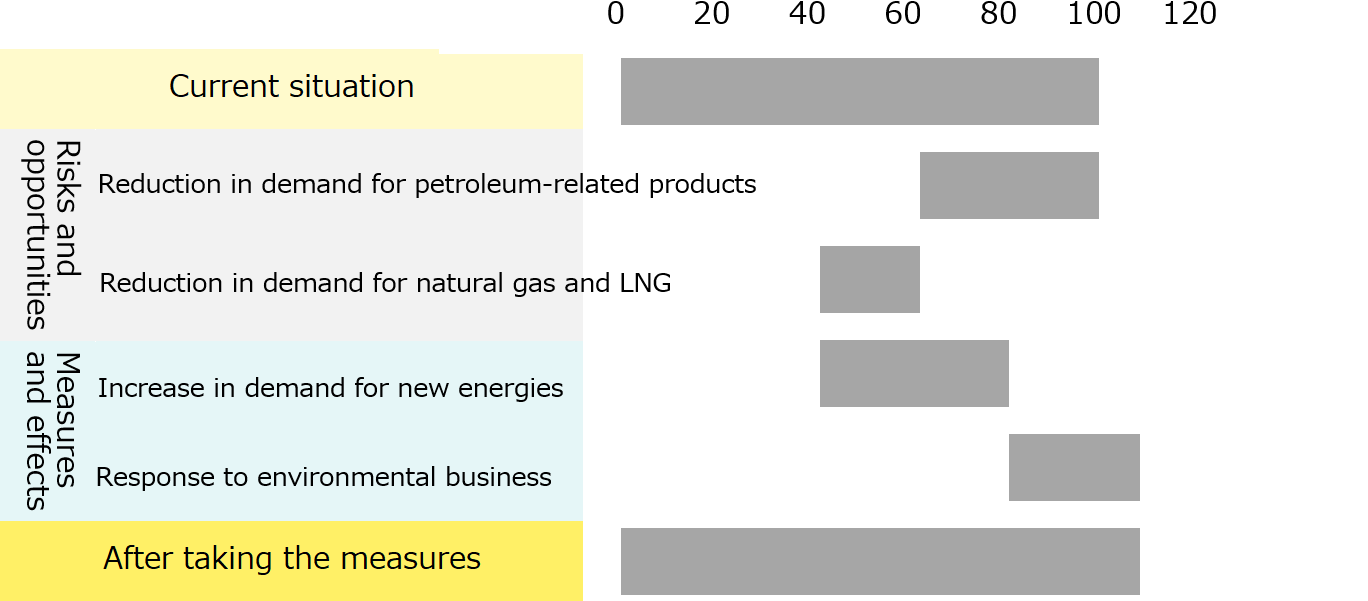

Risk: Countries may introduce regulations (e.g., carbon taxes) to realize a decarbonized society. This may cause global demand for oil to decrease. Demand for natural gas and LNG is also expected to shrink after 2030, but a certain level of demand for LNG as a transition fuel is expected to remain, especially in Asia

Opportunity: Demand for new energies (e.g., hydrogen, ammonia and renewable fuel) may increase as alternatives to fossil fuels

Opportunity: Business opportunities may increase for carbon dioxide capture, utilization and storage (CCUS) to reduce GHG

Physical

Risk: Production facilities could be damaged in a natural disaster (extreme weather)

Business environment under the scenario Business impact assessment

Under the 1.5℃ scenario, we expect global demand for oil to diminish and demand for natural gas and LNG to contract after 2030, but we aim to maintain and increase earnings by capturing opportunities to trade alternative fuels and develop new environmental businesses, such as CCUS. Although production facilities could be damaged due to natural disasters (extreme weather), the impact of damage is expected to be limited due to disaster countermeasures taken in cooperation with partner companies.

Analysis according to the profit after tax (%)

Adaptation/mitigation measures & policies

Business opportunities

We will focus our efforts on new energy, CCUS and other environmental businesses, and aim to restructure our energy business portfolio in line with the industrial structure in the decarbonization scenario.

Although demand for natural gas and LNG is expected to decline in the long term, we will continue to participate in projects and seize trade opportunities whilst taking into account societal needs, including the importance of natural gas as a raw material for hydrogen and a transitional fuel. As for our upstream petroleum-related assets, we will look to replace them and improve their efficiency in line with the decarbonization scenario.

Financial information

Profit in segment of applicable business (consolidated net profit): 35.9 bn yen (Energy Division/FYE 2025 Results)

Total assets in segment of applicable business: 1,652.0 bn yen (Energy & Chemicals Company/March 2025)

Timeframe

By 2030

Temperature Band Scenario

1.5℃ Scenario

Main risks and opportunities

Transition

Risk: Introduction and increase of carbon tax

Risk: Decrease in demand for virgin plastic due to widespread adoption of recycling

Opportunity: Increase in demand for low-carbon / decarbonization-related materials and products

Opportunity: Increase in demand for clean fuels and chemical raw materials

Physical

Risk: Damage to facilities / inventories and shutdown of operations caused by typhoons, floods, etc

Opportunity: Increase in demand for chemical materials and products related to production increase, preservation and stockpile of food

Business environment under the scenario Business impact assessment

Under the transition scenario, while the introduction and increase in carbon tax will increase costs and lower demand for virgin plastics will result in lower sales and profits, our chemical business will be able to increase earnings by capturing opportunities in environmental businesses such as recycled plastics, bioplastics, clean ammonia and methanol, where demand is expected to increase.

Analysis according to the profit after tax (%)

Adaptation/mitigation measures & policies

Business opportunities

Accelerate progress toward a decarbonized society through energy saving measures, procurement of renewable energy, etc.

Taking the initiative in realizing resource circulation by providing a 3R platform and sustainable cycle.

Restructuring our chemical business portfolio by accelerating our efforts in environment-related businesses, such as sourcing of environmentally friendly raw materials.

Financial information

Profit in segment of applicable business (consolidated net profit): 33.7 bn yen (Chemicals Division/FYE 2025 Results)

Total assets in segment of applicable business: 1,652.0 bn yen (Energy & Chemicals Company/March 2024)

2. Businesses for Which Physical Risks Are the Main Issues

The main issues for agriculture- and forestry-related businesses are physical risks in the 4℃ scenario.

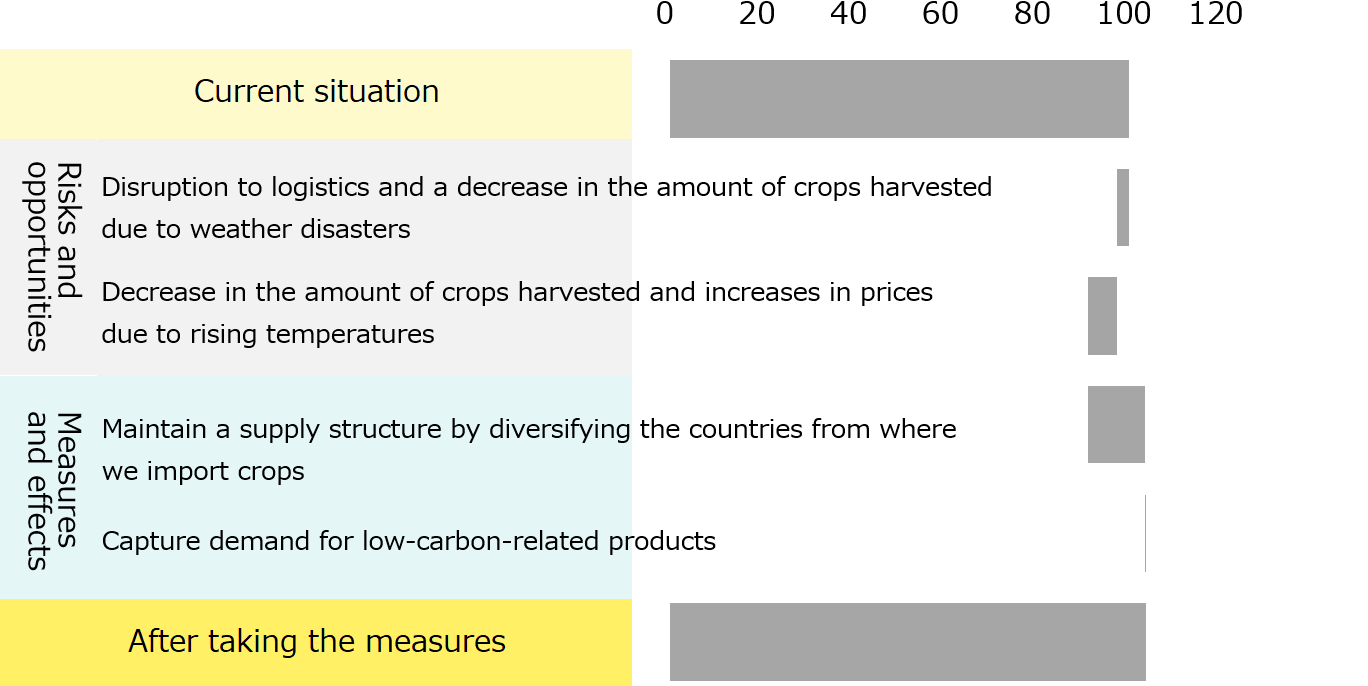

Opportunity: We may capture demand with feed products and other low-carbon-related products which contribute to reducing GHG

Physical

Risk: Decrease in the amount of crops harvested and logistics disruption due to large hurricanes, droughts and other extreme weather in countries from where we import crops

Risk: The amount of crops harvested may decrease and transaction prices may increase in countries from where we import crops due to rising temperatures

Opportunity: We may maintain a supply structure by diversifying the countries from where we import crops and capture demand for grain

Business environment under the scenario Business impact assessment

The decrease in the amount of crops harvested due to weather disasters and rising temperatures may lead to supply instability and increases in prices. However, we can maintain a supply structure by diversifying the countries from where we import crops and then provide further opportunities for low-carbon-related products.

Analysis according to the Gross trading profit indicator (%)

Adaptation/mitigation measures & policies

Business opportunities

We will diversify the countries from where we import crops to prepare for the acute and chronic impacts from climate change.

We will engage in new environmental-related business such as feed which leads to a curb on methane emissions.

Financial information

Profit in segment of applicable business (consolidated net profit): 33.3 bn yen (Provisions Division/FYE 2025 Results)

Total assets in segment of applicable business: 2,359.8 bn yen (Food Company/March 2025)

Timeframe

By 2030

Temperature Band Scenario

4℃ Scenario

Main risks and opportunities

Transition

Opportunity: Enhance the adoption of renewable energy solutions, such as solar power generation and biomass boilers, and the biogas power generation using in-house organic resources including residues from pineapple, banana and other fruit-base wastes

Physical

Risk: Reduction in harvest volumes due to extreme weather (floods, typhoons and droughts etc.) in banana and pineapple plantations in the Philippines

Business environment under the scenario Business impact assessment

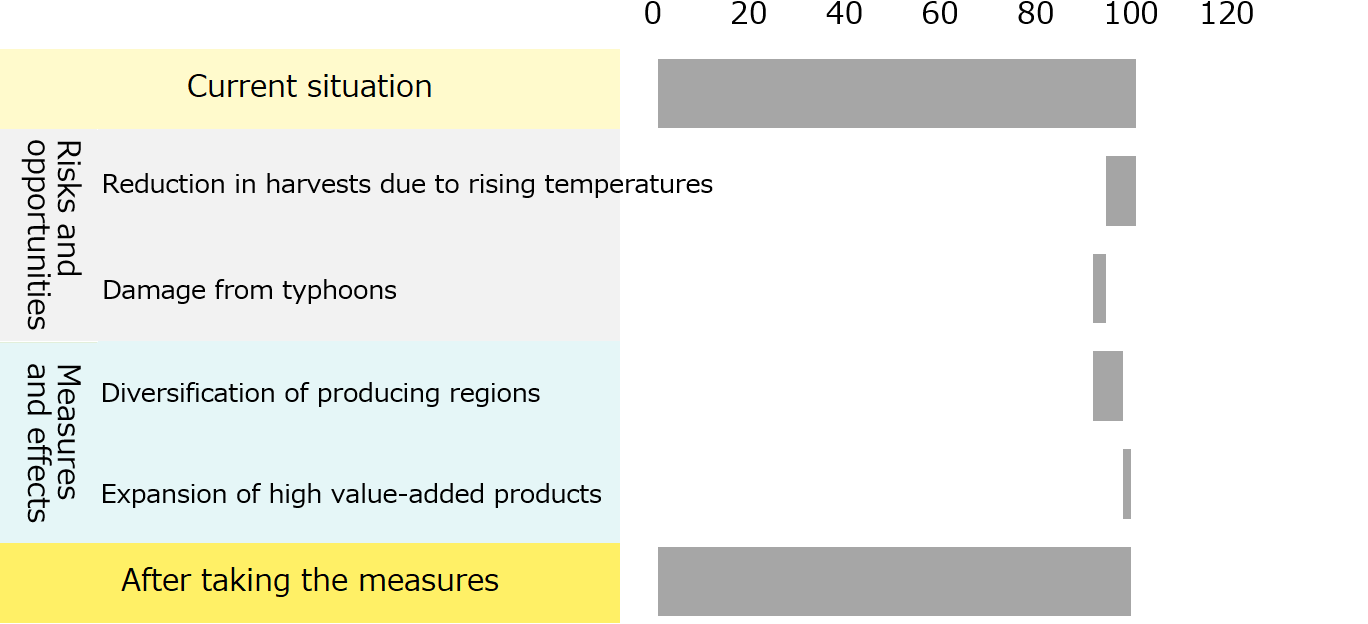

The decrease in harvest volumes attributable to extreme weather events can be mitigated by improving the unit yield through the development of resistant varieties and production methods (cultivation and irrigation etc.). We will diversify production areas and procurement sources (Sierra Leone and Vietnam etc.) for preparation against weather risks, and expand our portfolio of high value-added products. The above initiatives will make it possible to maintain earnings.

Analysis according to the EBITDA indicator (%)*

Earnings before interest, taxes, depreciation and amortization (This refers to earnings calculated by adding interest expenses and depreciation expenses to earnings before tax.)

Adaptation/mitigation measures & policies

Business opportunities

We will diversify producing areas and procurement sources in preparation for weather risks (Sierra Leone and Vietnam etc.).

We will increase unit yield by implementing advanced production methods, including the developing resistant varieties, improving seedling cultivation methods, and installing irrigation equipment.

We will use drones and ICT to increase the efficiency of production (agricultural chemical spraying location identification, yield prediction, and timely and accurate fertilization.)

We will contribute to low carbonization and water resource protection, capture the support of environmentally-conscious consumers and increase our brand value by expanding the introduction of recycling-based clean energies and renewable energies such as solar power.

We will expand our portfolio to include a diverse range of high value-added product offerings.

Financial information

Dole International Holdings net profit: (1.4) bn yen (FYE 2025 Results)

Total assets in segment of applicable business: 2,359.8 bn yen (Food Company/March 2025)

Timeframe

By 2030

Temperature Band Scenario

4℃ Scenario

Main risks and opportunities

Transition

Risk: Risk of the diversion of the use of timber to products other than paperboard products (competition in demand for timber)

Opportunity: Improvement in competitive advantage if the cost of carbon tax increases because we already use 100% biomass energy in pulp manufacturing

Opportunity: Preference for renewable and non-fossil resource-derived raw materials (timber)

Physical

Risk: Change in the suitable areas for growing trees for each species due to the temperature rise. Decrease in the amount produced depending on the species and region (pine trees throughout Finland and spruce trees in the south of the country)

Risk: Impact on procurement and production from rainstorms, droughts, floods, forest fires, pests, frozen soil thawing and other issues

Business environment under the scenario Business impact assessment

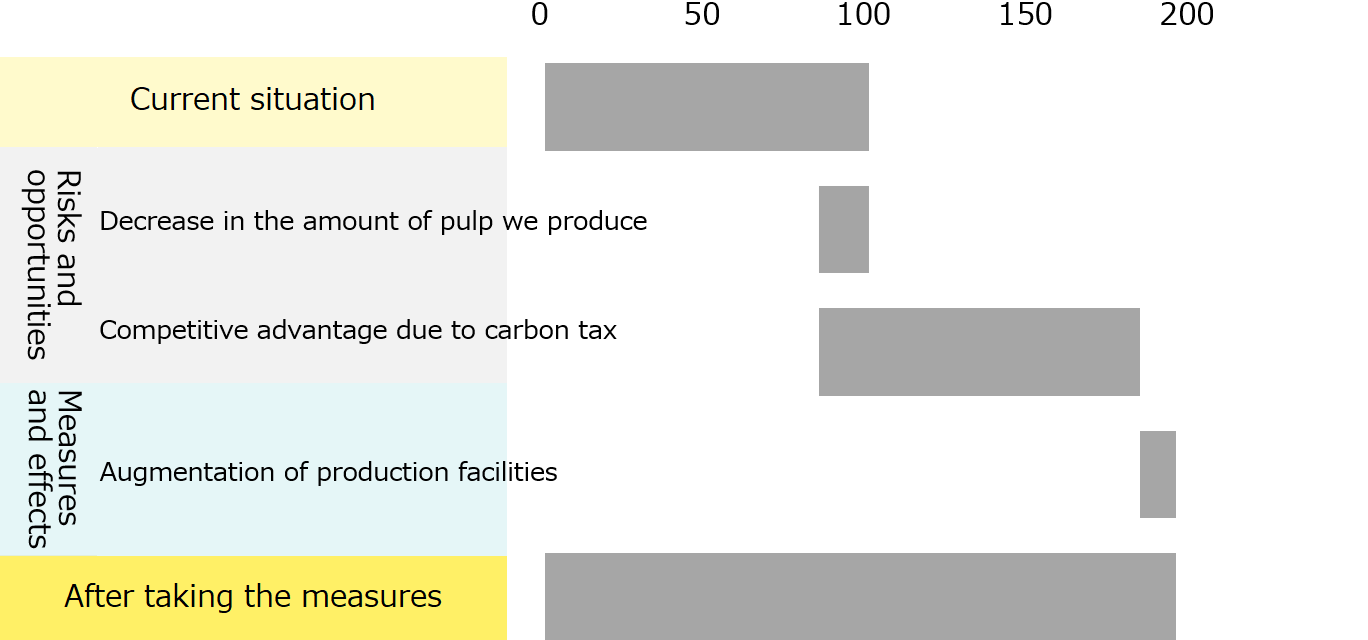

The amount produced is expected to decrease in some areas due to the rise in the global average temperature. Nevertheless, we can continue to improve earnings by increasing the amount of pulp we produce with the augmentation of facilities in afforestation regions where the amount produced is expected to increase.

Analysis according to the EBITDA indicator (%)*

Earnings before interest, taxes, depreciation and amortization (This refers to earnings calculated by adding interest expenses and depreciation expenses to earnings before tax.)

Adaptation/mitigation measures & policies

Business opportunities

We will utilize our strengths in the paper pulp business to contribute to the elimination of plastics and promote the launch onto the market of new materials which will contribute to sustainability. We invest in Paptic Ltd. in Finland and Transend Packaging Ltd. in the U.K. We continue development of cellulose nanofiber applications. Through such efforts, we will develop new markets in high value-added fields with forest-derived pulp serving as the main raw material.

The impact from the rise in temperature on the amount of pulp we produce will differ between northern and southern Finland. Accordingly, we will consider a production structure based on the location of afforestation regions and factories in Finland. We are planning to improve operating rates in northern Finland in particular with our minds focused on increasing the amount of pulp we produce. We made a large capital investment in a pulp factory in northern Finland through Metsä Fibre Oy in 2023 to raise production capacity (approximately 20% increase). We will aim for stable business operation by dispersing geographical risks relating to timber procurement and other areas through the dispersion of factory locations and production capacity.

Financial information

Profit in segment of applicable business (consolidated net profit): 30.2 bn yen (Forest Products, General Merchandise & Logistics Division/FYE 2025 Results)

Total assets in segment of applicable business: 1,475.0 bn yen (General Products & Realty Company/March 2025)

Impact on Existing Strategies and Business Transition Plans

During ITOCHU’s scenario analysis, we ascertained high-impact negative financial risks associated with not implementing climate change measures such as shifting current business strategy or business regions. As a result, we have been steadily promoting specific business transition plans and financial plans (including divestment and asset replacement) in line with our Management Policy “The Brand-new Deal” based on the basic policy of enhancing our contribution to and engagement with the SDGs through business activities.

Transition Plans for Main Businesses Subject to Transition Risks

In 2021, together with ITOCHU’s GHG emissions reduction targets, we announced our management plan to actively promote clean-tech business and other businesses that contribute to GHG emissions reduction as a way to enhancing contribution and engagement with the SDGs. This basic policy is carried over to the Management Policy “The Brand-new Deal” formulated in 2024. Through our own businesses, we aim to achieve a situation where the amount of our avoided emissions exceeds our GHG emissions by 2040.

Many innovative businesses leveraging cutting-edge technologies for decarbonization require time for fully social implementation. We are promoting businesses that contribute to emission reductions from a medium- to long-term perspective to achieve this goal.

Businesses Identified as Examples of Contributing to GHG Emissions Reduction and Strengthening Efforts toward the SDGs

Business

Summary

Environmentally Friendly Fibers

Contribution to a circular economy through expansion of sustainable materials.

Water and Waste Treatment

Developing businesses centered on Europe and the Middle East through collaboration with leading partners.

Operation of the world’s largest energy-from-waste (EfW) project in Dubai.

Renewable Energy

Promoting power generation businesses, including wind, solar, and geothermal, mainly in North America, Europe, and Asia.

Operating and providing maintenance services for solar power plants at approximately 1,400 locations in North America.

Recycling of Metal Scrap, etc.

Developing a wide range of recycling businesses of materials including metal scrap, by utilizing a nationwide network of recycling companies and providing waste management services.

Low-carbon Iron

Promoting the construction of a low-carbon iron supply chain that contributes to decarbonization of the steel industry.

CCUS (Carbon dioxide Capture, Utilization and Storage)

Collaboration with domestic and overseas business partners to commercialize the utilization of mineral carbonation technologies by Australia-based MCi.

Participate in a project commissioned by the New Energy and Industrial Technology Development Organization (NEDO), and also conduct R&D and demonstration projects for liquefied CO2 transportation technology.

Energy Storage Systems/ Renewable Energy

Promoting next-generation power services and environmental value trading by utilizing in-house brand AI-equipped ESSs and distributed solar power generation networks.

Developing next-generation batteries and promoting recycling-oriented businesses by reusing batteries for EVs.

Promoting renewable energy power sources, such as solar, biomass, and wind power.

Sustainable Aviation Fuel/ Renewable Diesel Fuel

Selling Sustainable Aviation Fuel (SAF) to airlines for the first time in Japan and promotion of renewable diesel.

Hydrogen and Ammonia

Promoting the establishment of a green hydrogen value chain in collaboration with Denmark-based Everfuel A/S.

Developing ammonia-fueled vessels and creating a proprietary operation model, developing a bunkering business, utilizing ammonia as an alternative fuel for power generation, and promoting manufacturing and marketing operations in Canada and elsewhere in order to build a value chain for clean ammonia.

Plastic Recycling

Developing plastic recycling businesses with leading partners boasting recycling technologies.

Product development using marine plastic waste as raw material.

Sustainable Coffee Beans and Vegetable Oil

Stably supplying sustainable products and third-party certified products to eliminate child labor and environmental damage.

Building raw material supply chains with established sustainability in production, distribution, and processing.

Production and Processing of Fruits and Vegetables/Waste Reduction

Reducing low-quality products and residues in the production, distribution, and processing of Dole products.

Sustainable Natural Rubber

Participate as a founding member in the global platform for sustainable natural rubber (GPSNR) to promote its production and use.

Developing PROJECT TREE, a traceability system using blockchain, involving the entire value chain.

Secondhand Mobile Phone Distribution

Entering the secondhand mobile distribution business by taking advantage of market trends such as excessive supply of new mobile phones and increased environmental impact due to mobile phone replacement.

CVS Business (FamilyMart)

Improving operational efficiency and reducing food loss through supply chain reforms.

Promoting FamilyMart Environmental Vision 2050, including efforts to reduce plastic use and GHG emissions.

Transition Plans for Main Businesses Subject to Physical Risks

In agriculture and forestry businesses, we aim to expand sustainable operations by adopting cutting-edge technologies from a medium- to long-term perspective and promoting the following initiatives.

Increase per-unit harvest volume by selecting breeds that are viable in high-temperature climates and improvements to production methods.

Expand business into other regions projected to see growth in production volume.

Financial Strategy

The Division Company Management Committee (DMC) conducts annual reviews of business risks and opportunities, including those related to climate change. Each DMC examines business transition plans, and then drafts annual financial plans. The annual financial plans for each Company are presented for approval to the HMC, the executive body, and the Board of Directors, the supervisory body, before final approval by the Board of Directors. This final approval is subject to a comprehensive analysis and deliberations from an ESG perspective, including matters related to climate change. In order to facilitate a financial strategy based on ITOCHU’s transition plan, we have developed a financing plan that limits the use of funds to projects that contribute to the SDGs.

SDGs Bond

In March 2021, ITOCHU issued SDGs Bond (Sustainability Bond totaling US 500 million dollars), which was allocated towards capital expenditures, manufacturing, R&D-related investments and procurement costs in climate-related subjects as well as R&D-related investments in procurement of certified food ingredients and costs of utilization of food residuals related to sustainable food systems like those indicated below:

Efforts to reduce GHG emissions: Renewable Energy (generation and storage)

Efforts to reduce GHG emissions in FamilyMart

Sustainable Food System: Expanding procurement of certified food ingredients and utilization of food residuals

Green Loan

In September 2023, ITOCHU entered into the green loan agreement with Sumitomo Mitsui Trust Bank, Limited, and in December 2024, with The Bank of Fukuoka, Ltd. The green loan will be used for our qualified projects (renewable energy power generation projects, energy from waste projects, and projects for the circular economy).

We confirmed that implementing these types of transition plans and financial strategy will enable us to maintain resilient business operations, even in over the medium- and long-term, for ITOCHU Group businesses, products, and services. Beyond the scope of applicability to this scenario analysis, ITOCHU is engaged in diverse business activities in various regions. Those business activities are also impacted by climate change. However, at this point of time, we have determined that the impact on Group overall earnings caused by risks associated with each individual business activity would be limited.

To confirm the impact of climate change on overall Group business, we will continue to conduct analyses of both transition and physical risks. We will further identify and organize fields susceptible to significant impact and evaluate response policies based on an order of priority given to areas requiring a response.

Risk Management

As a group engaged in global business operations, ITOCHU constantly monitors climate change policies in each country, the status of extreme weather around the world, and the business risks associated with changes in average temperatures. In the analysis of risks for our entire ITOCHU Group, we manage climate change risks identified based on an analysis of information concerning climate change measures, including regulatory information and extreme weather information, as one of the major risks (environmental and social risks) facing our company. Identified climate change risks are also examined and evaluated during our investment decision process. Each department in charge of risk management has established an organization for risk identification, evaluation, information management, and monitoring for the consolidated Group.

Identification and Evaluation of Climate Change Risks

ITOCHU considers those that may have a significant impact on the financial position and results of operations of the ITOCHU Group in the future as significant risks. We recognize risk management as an important management issue. Referencing the COSO-ERM framework, we outline our basic policy on risk management for ITOCHU and prepare the organizations and methods necessary for risk management.

Each Company and the Sustainability Management Division cooperate regularly to gather information to assess risk importance. This information includes trends in climate change policy and regulations, which mainly consist of existing and new regulations related to climate change in the countries in which we operate, climate-related technology, and clean-tech business. We also gather information on global extreme weather and average temperature increases. Importance is identified and assessed using specific indicators and from the perspective of ascertaining the substantive financial or strategic impact that climate risk may have on the Company. For example, for non-consolidated businesses, we identify an important risk as a risk that would cause a 10% change compared to previous fiscal year revenues, a 20% change in average net income for the most recent past five years, or a 30% change in net assets from the end of the previous year. For consolidated businesses, we would use a change of 10% from previous fiscal year revenues or a 3% change in total capital from the end of the previous year.

ITOCHU organizes the information we gather on climate change risks and opportunities into our Material Climate-related Risks and Opportunities (risk criteria), with analysis for both transition and physical risks. We use risk criteria to identify and assess climate change risks in the risk management process for each phase of business, including the start of a new business, existing businesses, handled products, supply chains, Group company business management, and business strategy reviews.

Climate change risks gathered during the risk assessment process are deliberated by the Sustainability Committee and other relevant committees to ensure we continuously review risk criteria and the risk identification process. During these deliberations, the relevant committees incorporate opinions received from the Sustainability Advisory Board, which promotes dialogue concerning sustainability between ITOCHU management and external stakeholders.

Integrating Climate Risk Management into the ITOCHU Group Risk Management System

Due to the nature of ITOCHU’s broad-based operations, we are subject to various risks, including market risks, credit risks, and investment risks. In addition to establishing various internal committees and designated responsible departments, we have created a risk management organizational structure and management methods necessary to address these risks. This organizational structure includes outlining management regulations, investment standards, risk limits, and transaction limits, as well as establishing structures for reporting and monitoring to enable integrated Group risk management.

Climate change risks are one of the major environmental and social risks subject to Group risk management. We incorporate this risk management into the assessment methods for each business phase shown in the table below, which can broadly cover our business activities as a general trading company including management of investment, trading products, logistics, Group companies, supply chain, business strategy, and portfolio, etc.

Climate-related Risk Management Procedures and Evaluation Methods for Each Business Phase

Please scroll sideways.

Business Phase

Evaluation Method

Business start

Environmental and social risk assessments including climate change risks for new investment project

Shadow pricing for carbon tax costs, etc., and stress test (internal carbon pricing)

Business management

Environmental risk assessments for handled products (LCA evaluation for overall supply chain)

Group company environmental status survey (2, 3 companies per year)

Supply chain sustainability surveys (supplier)

Internal environmental audits based on ISO 14001 (ITOCHU, 3 applicable Group companies)

Scope1/2/3 aggregation and year-on-year assessment

Internal carbon pricing impact assessment (e.g., US$205/t-CO2 in the case of power generation project (US))

Review business strategy

Consider business strategy, asset replacement

If risks and opportunities are identified via the evaluation methods at each business phase, we use the tool shown below in Risk Assessment & Management Activities to assess the impact of risks and opportunities on business. Risk Assessment & Management Activities include quantitative evaluations such as scenario analyses and stress tests, and qualitative evaluations such as assessments of compliance with investment policy and GHG reduction targets. Quantitative information for risks and opportunities not related to climate change is added to climate change risk and opportunity information that has been quantitatively assessed. This information is then used to analyze the level of contributions to earnings.

Risk Assessment and Management Activities

The TCFD scenario analysis identified the following risk and opportunity factors, as well as assessment and management activities.

Please scroll sideways.

Managed Factor

Risk and Opportunity Factors (example)

Evaluation and Management Activities (example)

Market

Decreased demand due to adoption of a carbon tax on energy (crude oil, gas, LNG) development projects

Increased LNG demand and increased demand for renewables and other new energy

Scenario analysis

Policy on climate change in relation to investment decisions

Conformity to ITOCHU GHG emissions reduction targets

Compliance with policy on investment and growth in new energy solutions

Earnings contributions

Regulations

Carbon tax on international transactions for energy and fuel

Adopt volume reduction requirements and emissions trading scheme (cap and trade scheme) in country of operation

Increased thermal power generation costs at power plants due to carbon tax and CCUS requirements

Scenario analysis

Portfolio stress test

Regulatory monitoring

Carbon prices

Conformity to ITOCHU GHG emissions reduction targets

Technology

Mobility electrification

Renewable energy and storage battery/lithium battery technology

CCUS, hydrogen/ammonia and other low carbon technologies

Digitized big data

Monitoring technological trends related to risk factors

Increased investment in new energy solutions, CCUS, and new low-carbon technologies

Digitization roadmap

Physical risks

Chronic effects (e.g., sea level rise, water scarcity increase)

Acute effects (e.g., more frequent extreme weather events)

Regular updates to meteorological and ocean data for new business development/existing business risk assessments

Updates to physical impact data on food products

Reputation

Maintaining company appeal in terms of personnel hiring

Investor awareness of climate change countermeasures

Climate-related lawsuits

Impact on acquiring licenses needed for business

Governance for climate change issues

Ensuring transparency of performance disclosure

Communication with stakeholders (investors, initiatives, NGOs, business affiliates)

ITOCHU has established a multilayered decision-making process that seeks to realize swift decision-making by delegating discretionary power to each internal Company, while pursuing investment returns and controlling investment risks. Depending on the size and terms of a project, a review is conducted at the internal Company level or by the Investment Consultative Committee and the HMC.

As a member of the HMC and the Investment Consultative Committee, the CAO, who also serves as chair of the Sustainability Committee, participates in the screening of projects that exceed the authority of the Division Company President. This system reflects the content of deliberations at the specific stage of climate change risk and at the assessment stage of climate change risk for company-wide risk management.

ITOCHU evaluates and manages risks such as climate change, natural disasters, and ESG investment identified in the business start stage and the business management stage through collaboration between responsible committees such as the Sustainability Committee and Internal Control Committee and a system of periodic monitoring and review of ITOCHU Group companies. Environmental and social risks, including climate change, are summarized as one of the major risks subject to centralized management. Each year, the Sustainability Management Division serves as the executive unit in charge of organizing this information and issuing reports to the Internal Control Committee along with information on the other major risks to integrate the risk information into company-wide risk management system. The Sustainability Committee also deliberates on policies and measures related to climate change risk and how to promote the risk management system, etc. The director serving as chair of the Sustainability Committee reports on the content of deliberations to the Board of Directors approximately twice per year.

As part of our specific climate-related risk management procedures, we compile the results of Scope1/2/3 for each of 8 Division Companies every year. The results are compiled in a form that allows for an assessment over time, and are reported to the Sustainability Committee and the Board of Directors after being approved by each Division Company. This process enables the Board of Directors to oversee progress toward achieving GHG emissions reduction targets from a medium- to long-term perspective, and is also used to review new business strategies.

In order to achieve our GHG emissions reduction targets, we promote climate change initiatives through dialogue with suppliers, sales clients, contractors, and business partners in our value chain.

Review Business Strategy

Reviews of business strategy related to climate change are conducted by DMC, and then by the HMC via the Investment Consultative Committee on which the CAO, who serves as the chair of the Sustainability Committee, also participates as a key member. Final decisions are made following deliberation by the Board of Directors. Scenario analysis based on TCFD recommendations is also used as a tool when considering business strategies and asset replacement. In ITOCHU’s analysis, we analyze short-term, medium-term, and long-term climate-related risks and opportunities once a year for their impact on organization business, strategy, and financial planning.

Metrics and Targets and Action Plan

ITOCHU has set the following targets for GHG emissions, electricity usage, and clean-tech business as part of our response to climate change risks and opportunities. When setting these metrics and targets, we reference, among others, the Paris Agreement, Japan’s NDC and IEA materials, which are highly recognized internationally and can cover a wide range of business areas.

GHG Emissions Reduction Targets

Metrics (aggregation range): Scope1/2/3 (ITOCHU and subsidiaries), fossil fuel business and interests (ITOCHU, subsidiaries, equity and general investments)

Targets:

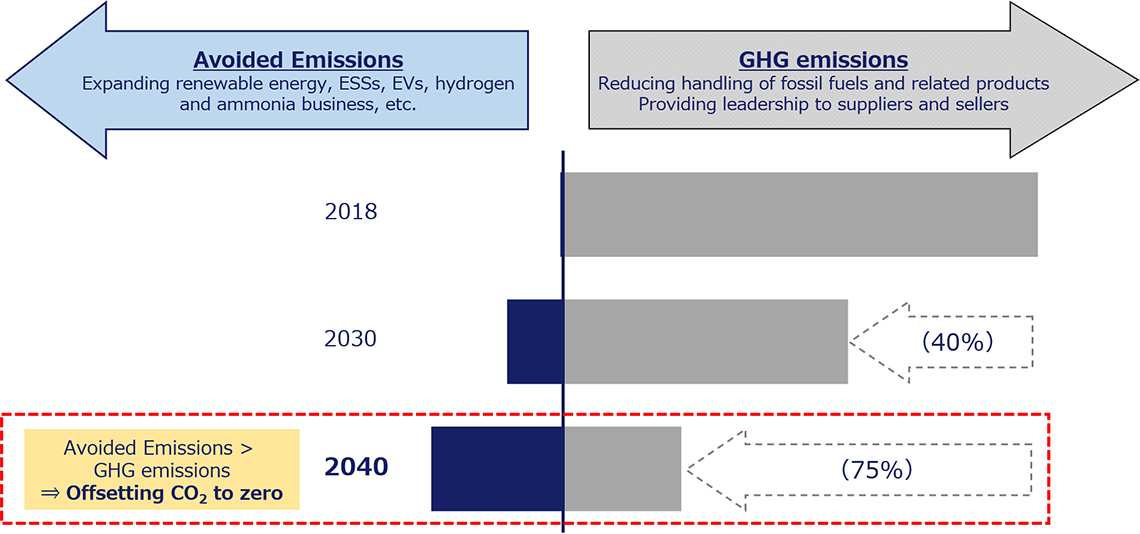

Achieve net zero GHG emissions by 2050.

Achieve 75% reduction from 2018 levels by 2040, aim for “offset zero”* through aggressive promotion of businesses with avoided emissions.

Offset zero: When avoided emissions exceed company GHG emissions

ITOCHU has set a short-term target of reducing Scope1/2 emissions at our Japanese Bases. We have registered such target with the GX League, a group of companies challenging the green transformation led by Japan’s Ministry of Economy, Trade and Industry in collaboration with the Japanese government and academia. We also participate in the Carbon Credit Market of Tokyo Stock Exchange, which will be used in the GX League, and contribute to the decarbonization of our own and other companies.

Please scroll sideways.

(Unit: t-CO2e)

FYE 2022 (Base Year)

FYE 2024-2026 Total (Target)

FYE 2026 (Target)

Scope1

77

223

74

Scope2

5,946

17,308

5,711

Scope1+2 Total

6,022

17,531

5,785

The scope of calculation is based on the “the Rules for Phase 1 in the GX-ETS” and does not match Scope1/2 for Japanese Bases of ITOCHU as a whole.

Clean-tech Business Metrics and Targets (Action Plans)

We set the following metrics and targets (Action Plans) in ITOCHU Clean-tech Business as one of the main metrics (benchmarks) for climate-related risks and opportunities.

In the power generation business, increase project development towards the goal of increasing our rate of renewable energy (equity interest basis) to over 20% by FYE 2031.

Build a next-generation fuel value chain based on hydrogen and ammonia.

Create distributed power supply platform using AI storage batteries boasting the No.1 sales in Japan. (Aim for scope exceeding cumulative power storage of 2 GWh by FYE 2031.)

Address Climate Change (Contribute to a Decarbonized Society)

Climate Change Opportunities

Taking countermeasures against climate change

Overall power generation business

We will develop power plants with a good balance between renewable energy power generation and conventional power generation, thereby contributing to the development of countries and regions in a sustainable manner that is optimized for each.

Pursue opportunities to invest aggressively in renewable energy power generation through analyses of countries and regions.

FYE 2031: Target to achieve a renewable energy ratio more than 20% (equity interest basis) and reflect this to the future strategy.

Tyr Energy Development Renewables, a renewable energy development company established in FYE 2023, is currently developing 25 assets with a capacity of 5GW of solar power in the United States.

The U.S. wholly owned subsidiary, NAES Corporation, the world’s largest independent power plant operation and maintenance service company, provides asset management and operation & maintenance services for approximately 1,400 sites, including 2GW of solar power plants and 1.1 GW of wind power plants in the renewable energy sector.

In June 2023, the US renewable fund was established. Through the fund, the first investment was made in a wind power plant in February 2024. Additionally, in September 2024, the second investment into solar and battery energy storage assets was agreed.

As of March 2025, the ratio of renewable energy based on generation capacity share is 18.7%. (1.6% increased compared to the previous year)

Address Climate Change (Contribute to a Decarbonized Society)

Evolve Businesses through Technological Innovation

Climate Change Opportunities

Innovation

Taking countermeasures against climate change

Next-generation business development

Ships/Shipping field

We will contribute to decarbonization in the shipping and maritime sectors through the promotion of an integrated project encompassing the development, ownership and operation of ammonia-fueled ships, the development of fuel supply chains, and fuel procurement.

In addition to the joint development of ammonia-fueled vessels with the Japanese consortium and the ownership and operation of these vessels, ITOCHU will take the lead in the development of supply chain of an ammonia bunkering and fuel procurement, aiming for early materialization of the pilot project.

After 2027, promote the spread of ammonia-fueled vessels and the establishment of a supply chains to contribute to the decarbonization of the maritime industry.

To contribute to decarbonization in the shipping sector, we are developing an integrated project aimed at: (i) developing ammonia-fueled vessels, (ii) owning and operating ammonia-fueled vessels, (iii) establishing fuel supply chains, and (iv) procuring/producing clean ammonia.

Test operation of first commercialized engine (for ammonia fueled large bulk carrier as our pilot project) with ammonia as a fuel was started from February 2025 at engine maker in Japan. Once the engine development progresses to a certain extent, discussions with relevant parties will be accelerated towards the order of the ship.

Selected by the Singapore government as a potential bunkering operator in July 2024. Discussions, including the ordering of bunkering vessels, are ongoing towards the establishment of a bunkering business in the country. And the bunkering business in Spain is being promoted in collaboration with Peninsula Petroleum.

In August 2024, the green ammonia production project utilizing existing ammonia facilities in Indonesia, jointly promoted with PUPUK Indonesia and Toyo Engineering, was selected as a target project for the Global South subsidy. Following the execution of the Front-End Engineering Design (FEED), discussions with relevant parties are ongoing towards the investment decision in FYE 2026.

Address Climate Change (Contribute to a Decarbonized Society)

Evolve Businesses through Technological Innovation

Climate Change Opportunities

Innovation

Taking countermeasures against climate change

Next-generation business development

Sales of passenger cars and commercial vehicles

We will achieve the eco-friendly mobility society by strengthening businesses of electric vehicles (EVs), hybrid vehicles (HVs), vehicles with a reduced environmental impact, and those related.

Contribute to spread of eco-friendly vehicles by increasing business of eco-friendly and high-efficiency products, such as EVs, HVs, vehicles with a reduced environmental impact, and related parts.

Expand sales of eco-friendly products in response to the expanded lineup of EVs, HVs, vehicles with a reduced environmental impact, and similar vehicles from automakers as our business partners.

As a partner in EVision, Isuzu’s total solution program for EVs, we have expanded our efforts to promote commercial EVs. In collaboration with iGRID Solutions Inc., we initiated a demonstration project in October 2024 to integrate EV operations with facility energy management.

In the Ministry of the Environment’s commissioned project, Demonstration Project for Sector Coupling through the Combination of Battery Swapping EV Development and Renewable Energy Utilization, we achieved over 45,000km of cumulative deliveries. (25,000km increased compared to the previous year) As planned, the delivery demonstration operation concluded in December 2024. And we conducted an examination of the business model aimed at promoting the widespread adoption of EV trucks by eliminating charging time constraints through battery swapping.

Address Climate Change (Contribute to a Decarbonized Society)

Water Resources

Pollution Prevention and Resource Recycling

Improving water and sanitation infrastructures

Water and environmental projects

We will contribute to improve the sanitary conditions, the development of economic activities, and the protection of the global environment through the appropriate treatment and effective use of water and waste.

Expand water and environment projects to promote the appropriate use and treatment of water and the effective utilization of resources, and reduce the burden on the environment.

Expand the investment portfolio in the water and environment field which contribute to social demands for the environment and the promotion of a circular economy.

Water Field

We are promoting seawater desalination business in Australia and Oman.

Environmental Field

UK: Our operations encompass three municipal solid waste incineration and power generation facilities (Energy-from-Waste/EfW plants), processing 850,000 tons of waste annually. These plants provide electricity for 100,000 British households equivalent.

Serbia: We set up first integrated waste management system in the Republic of Serbia. It contributes to the environmental issues such as greenhouse gases (GHG) (CO2 equivalent) emission and polluted water leakage due to the inappropriate waste treatment. We have initiated an integrated waste management operation, including an EfW facility from July 2024. The project anticipates a reduction of approximately 210,000 tons of GHG emissions and has received Certification of Carbon Credit from the Gold Standard.

UAE: We are currently operating the first EfW project in Dubai. These facilities are designed to process half of the Dubai’s municipal solid waste annually (1.9 million tons). The construction of this plant, the largest of its kind in the world, was successfully completed in August 2024.

Saudi Arabia: We are actively engaged in integrated hazardous waste management services in Jubail Industrial City.

Address Climate Change (Contribute to a Decarbonized Society)

Climate Change Opportunities

Innovation

Taking countermeasures against climate change

Next-generation business development

Aerospace business

To achieve decarbonization in the aviation industry through the adoption of hydrogen fuel cell engines

To commercialize hydrogen fuel cell engines, we aim to enhance public acceptance by collaborating with hydrogen-related companies, including the development of hydrogen infrastructure

Targeting the commercialization of the ZA600 engine, which can be installed on small aircraft, from 2026 onward. Following that, the ZA2000 engine — suitable for larger turboprop aircraft — is planned for development and commercialization.

Newly added from FYE 2026.

Metals & Minerals Company

Address Climate Change (Contribute to a Decarbonized Society)

Evolve Businesses through Technological Innovation

Climate Change Opportunities

Capital Introduction

Innovation

Taking countermeasures against climate change

Next-generation business development

Resource recycling business

Mining business

Environmental business

Materials-related business

We will realize stable resource supply as our social mission and responsibility while fully considering its environmental impact.

We will contribute to climate change issues through businesses that help to reduce greenhouse gases (e.g., lighter-weight vehicles and electric vehicles (EVs)) and the stable supply of essential materials.

Take the lead in developing recycling-orientated business.

Promote initiatives for the social implementation of hydrogen and ammonia, etc. as resources and raw materials that contribute to the decarbonization in client industries (e.g. steel and power).

Promote businesses to contribute to the stable supply of nickel, PGM and other materials necessary in the manufacture and supply of hydrogen, green materials and energy, and storage batteries.

Continue to be involved in the development of technologies that contribute to the reduction of greenhouse gas emissions, including technologies for carbon dioxide capture and storage (CCS) and carbon dioxide capture and utilization (CCU).

Promote initiatives to completely withdraw from thermal coal mine interests while continuing to realize stable resource supply as our social mission and responsibility through trading in regards to our coal business.

Implementation and expansion of businesses that contribute to developing lighter-weight vehicles and shifting to EVs (e.g., aluminum and copper).

Promote recycling-orientated business.

Promote initiatives for the social implementation of hydrogen and ammonia, etc. as resources and raw materials that contribute to the decarbonization in client industries (e.g., steel and power).

Promote examination toward technological development and commercialization to contribute to a reduction in greenhouse gas emissions, including hydrogen, green material and energy production, and carbon dioxide capture and storage (CCS) and carbon dioxide capture and utilization (CCU).

Strive to withdraw from thermal coal mine interests.

Realize initiatives in businesses that contribute to developing lighter-weight vehicles and shifting to EVs (e.g., aluminum and copper).

Together with JFE Steel, UAE’s largest steelmaker EMSTEEL, and others, we have promoted detailed feasibility studies for the establishment of a supply chain of ferrous raw material for green ironmaking with low carbon emission, which contribute to the decarbonization of the steel industry. In May 2024, we signed a Memorandum of Understanding with CSN Mineração S.A. [CM] in our Iron Ore Business in Brazil and NEXI concerning the decarbonization of the steel industry, which includes utilizing high-grade iron ore produced by CM.

We are contributing to the effective utilization of limited resources and the supply of environmental materials by promoting 3R+W (reduce / reuse / recycle + waste management). Specifically, we are steadily promoting initiatives in venous industries. This includes the reuse and recycling of store facilities and fixtures, the expansion and increase in sophistication of metal scrap and waste treatment through the use of a nationwide network of recycling companies.

We have invested in Everfuel of Denmark, who conducts the design, EPC, and operation of green hydrogen production facilities, distribution assets, and operation of hydrogen stations by using water electrolysis equipment, as well as the sale of hydrogen. In February 2025, we have commenced the first commercial production of green hydrogen, promoting the establishment of a locally-produced and consumed green hydrogen value chain.

We are promoting the Platreef project and others in the PGM (platinum group metals)/nickel business where demand is expected to grow significantly due to the worldwide spread of electric vehicles and fuel cell vehicles, and also expanding trade activities of such materials.

We have an investment into Australia-based MCi, who possesses mineral carbonation technologies. We are promoting their technology for the market. In December 2024, we have completed the construction of the first demonstration plant capable of processing multiple raw materials such as waste concrete and steel slag to produce carbonates. In January 2025, we have signed a memorandum of understanding with Mitsubishi UBE Cement Corporation to promote the construction of manufacturing plants and the establishment of a supply chain for raw material procurement and sales.

Agreement was signed with KOKO Networks, a Climate Technology Company Operating in Kenya, to support the generation of high quality carbon credits. In 2024, the first credits from our project with KOKO have been produced, and joint sales have been promoted.

Steadily promoted aluminum trade business that contributes to automobile weight reduction and electrification. We have traded approx. 500,000 tons in FYE 2025, and promoted sales of environmentally friendly raw materials for aluminum.

We decided to withdraw from thermal coal mine interests with a perspective of strengthening contribution and initiatives to SDGs. We already divested our Drummond mine interests in Colombia that had accounted for the majority of the ITOCHU’s thermal coal interests and also divested Ravensworth North coal mine interests in Australia producing both thermal and coking coal.

Energy & Chemicals Company

Address Climate Change (Contribute to a Decarbonized Society)

Transition Risk

Stable Supply of Resources

Stably supplying energy taking into account climate change and the environment

Oil/gas interests and liquefied natural gas (LNG) projects

We will produce resources (transition fuels) taking into account a reduction in greenhouse gases. We will provide a stable supply of energy to contribute to the development of industry and the construction of infrastructure.

Work on resource development projects in collaboration with superior partners who have advanced technical capabilities and abundant experience.

Pursue opportunities to participate in gas projects with a relatively low environmental burden in fossil fuels and as raw material source of the low-carbon fuel while keeping in mind the stable supply of energy in the transition phase toward the realization of a sustainable society.

To realize a sustainable society through the stable supply of energy, we continue to discuss with competent partners ways to participate in new upstream projects and collaborate on decarbonization as raw materials for a transition fuel.

Address Climate Change (Contribute to a Decarbonized Society)

Climate Change Opportunities

Energy use that takes into consideration local communities and the environment

District heating and cooling

We will promote initiatives toward environmentally friendly regional energy use.

Communicate appropriately with neighboring stakeholders in the Jingu Gaien district.

Engineering, construction, and operation of highly efficient heat supply plants.

Maintain the stable operations of district heating and cooling in the Jingu Gaien district and promote the district heating and cooling to neighboring areas.

We are continuing discussions with the relevant stakeholders to spread and promote district heating and cooling to neighboring areas.

Address Climate Change (Contribute to a Decarbonized Society)

Climate Change Opportunities

Efforts to optimally and continuously supply renewable energy

Energy Storage System

Power and Environmental Solution

We will continue to stably supply the Energy Storage System that are the key to the efficient and optimal utilization of renewable energy.

We will continue to sell Energy Storage Systems equipped with optimal charge and discharge software based on machine learning (AI).

Composition of PV integrated storage systems and power storage facilities.